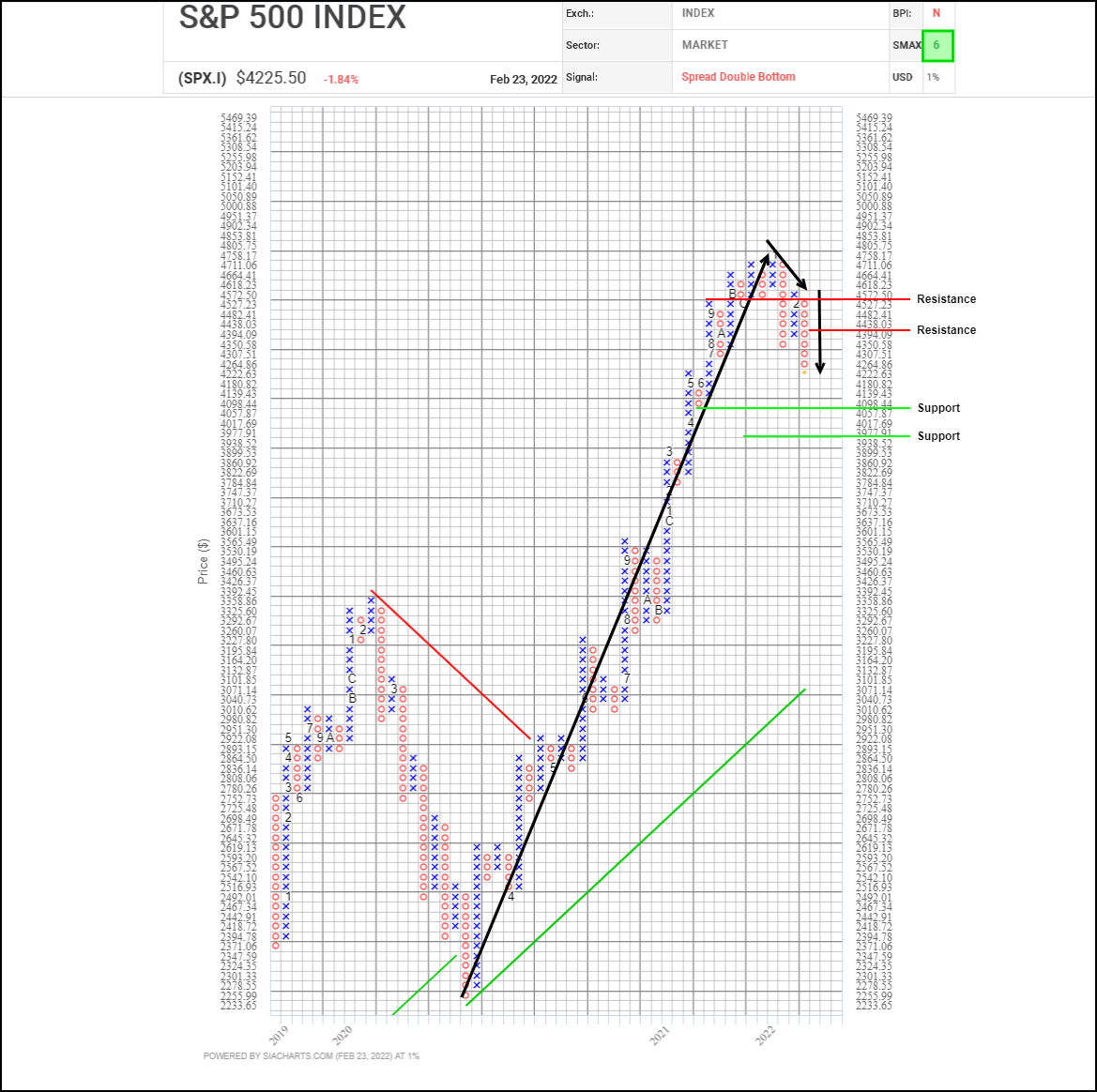

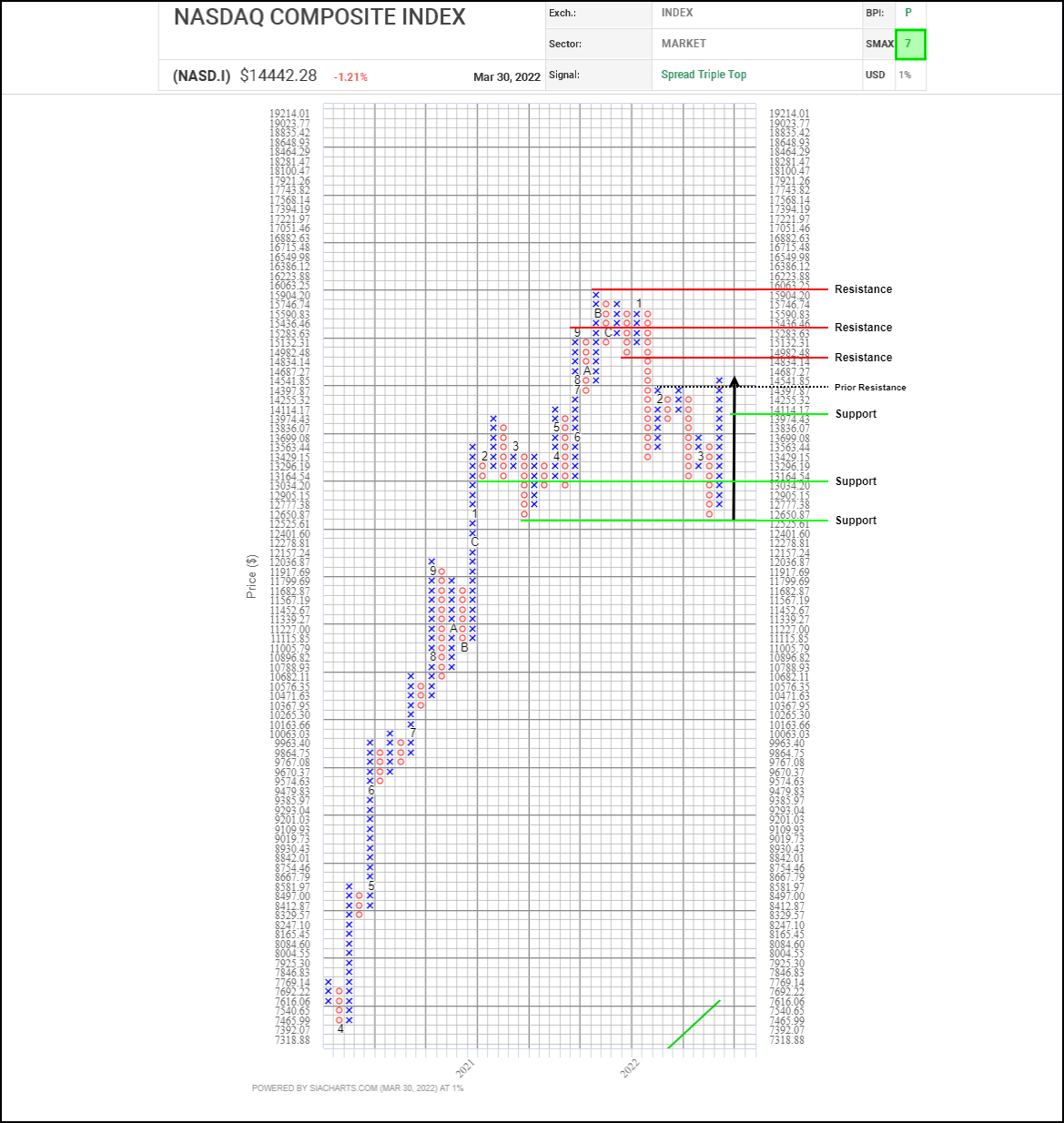

The rebound in US and European stock markets which started tentatively last week has accelerated this week. With peace talks between Russia and Ukraine continuing, some of the darkest fears which had gripped markets through February and the first part of March have eased a bit, enabling some of the more depressed areas within equities to rebound including European indices, small caps, and technology/communications stocks.